Understanding ISA 700: The Auditor’s Report on Financial Statements

Wanna know what makes an audit report stand out? How does an auditor ensure that their opinion on a company's financial statements is conveyed with clarity and credibility? Let’s dive into ISA 700, which provides auditors with the framework for drafting their opinion on financial statements.

The auditor's report is more than just a formality—it's the backbone of trust in financial reporting. ISA 700 ensures that every report is not only clear and consistent but also reveals the key insights that stakeholders need. Transparency, credibility, and professional judgment come together to form an audit report that investors, regulators, and management can rely on.

What is ISA 700?

ISA 700 – The Auditor’s Report on Financial Statements is a crucial standard issued by the International Auditing and Assurance Standards Board (IAASB). It governs how auditors should prepare and express their opinions regarding the financial statements of an entity. The primary aim of ISA 700 is to ensure that the auditor’s report is clear, informative, and accurately reflects the findings from the audit.

In essence, the auditor’s report is the final product of the audit process. It’s the document that communicates to stakeholders, including investors, regulators, and management, whether the financial statements give a true and fair view of the company’s financial position.

Key Elements of ISA 700

ISA 700 defines a structured approach to ensure that the auditor's report is both consistent and comprehensive. Let’s break down the key elements:

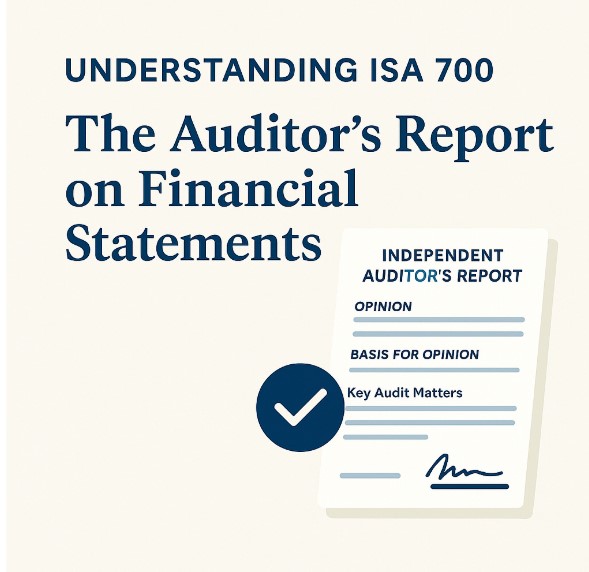

- Title and Addressee: The report must begin with a clear title that identifies it as an independent auditor’s report. The addressee typically includes the entity’s shareholders or board of directors.

- Auditor’s Opinion: The most important part of the report is the auditor’s opinion. This section reflects whether the financial statements are free from material misstatement and whether they provide a true and fair view of the company's financial position. The opinion could be one of the following:

- Unmodified Opinion (Clean Opinion): The financial statements are presented fairly.

- Qualified Opinion: There is a material misstatement but not pervasive.

- Adverse Opinion: The financial statements do not present a true and fair view.

- Disclaimer of Opinion: The auditor is unable to form an opinion.

- Basis for Opinion: This section outlines the audit procedures and the reasons for the auditor’s opinion. The auditor must clearly explain the standards followed, including relevant auditing frameworks and any limitations encountered during the audit.

- Key Audit Matters (KAMs): ISA 700 requires the auditor to communicate any Key Audit Matters (KAMs). These are matters that, in the auditor’s professional judgment, were of the most significance during the audit. KAMs often highlight areas with high risks of material misstatement, complex judgments, or significant changes in accounting policies.

- Responsibilities of Management and Those Charged with Governance: This section outlines management’s responsibility for preparing the financial statements in accordance with applicable financial reporting frameworks (e.g., IFRS or GAAP) and ensuring their accuracy.

- Auditor’s Responsibility: The auditor’s responsibility section emphasizes their role in expressing an opinion based on the audit. It also clarifies that the auditor is not responsible for the preparation of the financial statements, which lies with the management.

- Signature and Date: The audit report must be signed by the auditor (or audit firm), indicating who conducted the audit and when it was completed.

Why is ISA 700 Important?

The auditor's report is a vital tool for all stakeholders in the financial ecosystem, and ISA 700 ensures it’s reliable, consistent, and objective. Here’s why it matters:

- Credibility: It provides a high level of trust in financial reporting by offering an independent third-party validation of the financial statements.

- Transparency: ISA 700 ensures that all significant issues, including KAMs, are disclosed, fostering a more transparent financial environment.

- Consistency: By standardizing the format and content of the report, ISA 700 ensures that auditors around the world produce reports that are easily understandable and comparable.

What Can Go Wrong? Common Challenges

While ISA 700 ensures standardization, there are challenges auditors face in applying the standards:

- Judgment: Some decisions require significant professional judgment, especially when identifying Key Audit Matters.

- Complex Entities: For large organizations with complex structures, the audit might involve complex accounting issues, which can make the report harder to understand for users without deep financial knowledge.

- Going Beyond the Report: The auditor’s report can only provide so much information. Stakeholders often want more detailed insights into a company’s financial health, and this could lead to communication gaps.

Conclusion: The Importance of ISA 700 for Stakeholders

ISA 700 is the backbone of the auditor’s report, ensuring that it delivers clear, reliable, and comprehensive information to users of financial statements. Whether you’re an investor, regulator, or corporate stakeholder, understanding the role and components of this report helps you make more informed decisions.

For auditors, ISA 700 is essential in maintaining the integrity of the auditing profession and upholding the public trust in financial reporting.

Key Takeaways:

- ISA 700 provides a framework for auditors to express their opinion on financial statements.

- It includes key components like auditor’s opinion, basis for opinion, and Key Audit Matters (KAMs).

- The auditor’s report ensures transparency and credibility in financial reporting.

How does ISA 700 ensure transparency and credibility in the auditor's report on financial statements?