Deferred Tax Liabilities on Fair Valuation – A Hidden Time Bomb?

Wanna show stronger financials through fair value gains?

Be careful. You might be quietly loading a time bomb into your balance sheet.

In the world of IFRS reporting, fair valuation is celebrated for enhancing transparency and aligning financials with economic reality. It brings global consistency and boosts stakeholder confidence. But here’s the twist — while the asset side of your balance sheet may look healthier thanks to fair value adjustments, the equity side quietly absorbs a hit through Deferred Tax Liabilities (DTLs).

And if these DTLs are not properly assessed or managed, they can trigger serious consequences for valuation, compliance, and long-term strategic decisions.

In a world where unrealised gains are applauded, Deferred Tax Liabilities are often ignored — until they become a problem. They reduce retained earnings, alter perception, and affect key financial decisions. And the worst part? These liabilities may never reverse, yet they continue to weigh down your balance sheet.

📘 What Is Fair Valuation and Why It Matters

Under various IFRS standards — including IFRS 9 (Financial Instruments), IFRS 13 (Fair Value Measurement), IFRS 3 (Business Combinations), IAS 40 (Investment Property), and IAS 16 (PPE) — companies are required (or allowed) to measure certain assets at fair value.

This gives a more accurate snapshot of the financial position. However, the tax base of these assets generally remains unchanged until realisation. The difference between the carrying amount and tax base creates a temporary difference, which triggers Deferred Tax Liabilities under IAS 12.

🧠 Understanding Deferred Tax Liabilities (DTLs)

A Deferred Tax Liability arises when:

The accounting value of an asset exceeds its tax base, and the difference is expected to reverse in the future.

Even if this reversal will only occur upon sale — or not at all — IAS 12 generally requires recognition of a DTL on that temporary difference.

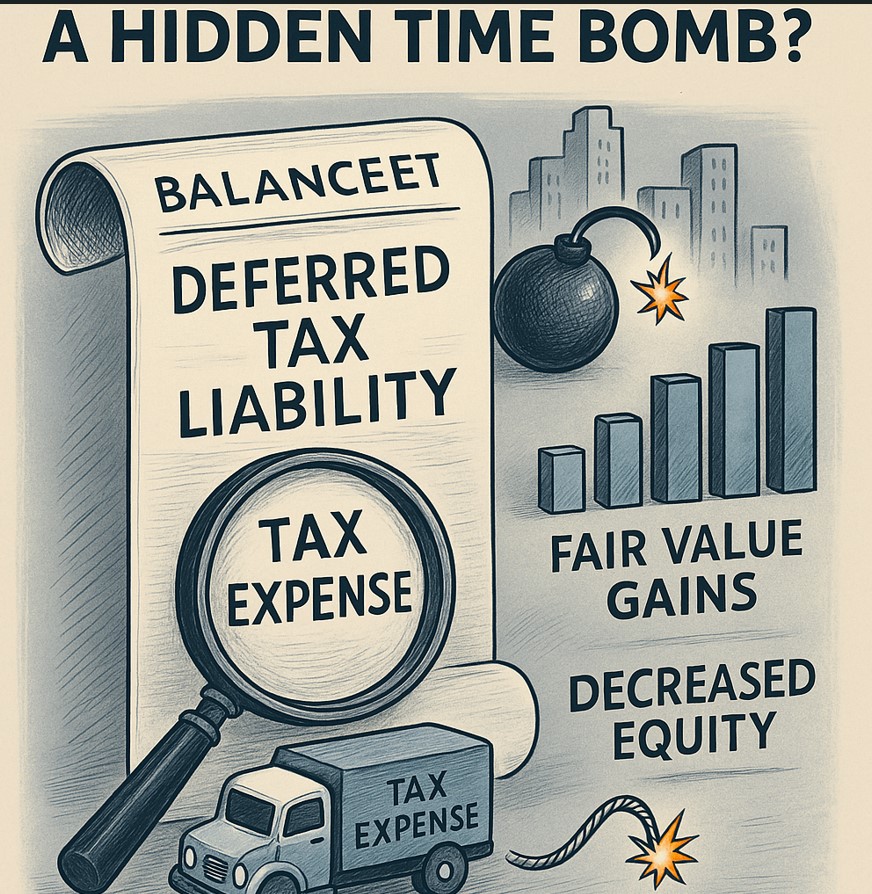

⚠️ The Fair Value Trap – An Illustration

Imagine a company holds an investment property initially recorded at €1 million. Over time, the asset is fair valued at €2 million under IAS 40.

- 📈 €1 million gain on the balance sheet

- 💼 No real transaction — it’s unrealised

- 📉 €250,000 DTL recorded (assuming 25% tax rate)

Profitability on paper improves, but equity takes a hit through the DTL. And if the asset isn’t sold for years — or ever — that liability just sits there, quietly distorting the financial picture.

🔍 The Real Dangers of DTL on Fair Valuation

- Impact on Net Equity and Financial Ratios: DTLs reduce retained earnings and equity, skewing solvency and leverage ratios.

- Disconnect Between Book Gains and Cash Reality: Unrealised gains show up in profits, but DTLs affect equity with no cash impact.

- Dividend Distribution Implications: DTLs reduce the reserves from which dividends can be safely paid.

- Impact on M&A and Due Diligence: DTLs reduce net asset value, lowering deal value during acquisitions.

- Possible Non-Reversibility: For long-term assets, temporary differences might never reverse, yet the liability remains.

🤔 Should All DTLs Be Recognised?

IAS 12 is fairly strict: if a taxable temporary difference exists, a DTL must be recognised unless:

- It arises from initial recognition of goodwill

- It stems from initial recognition of an asset or liability in a transaction that is not a business combination and affects neither accounting nor taxable profit

Outside of these exceptions, recognition is generally mandatory — but with planning, its impact can be minimised.

📌 Practical Tips to Manage DTL Risks under IFRS

- Choose Fair Value Models Judiciously: Where optional, avoid fair value unless strategically beneficial.

- Improve Financial Statement Disclosures: Clarify realised vs. unrealised gains and the role of DTLs.

- Consider FVOCI Classification: Some instruments under IFRS 9 can be classified to better manage DTL impact.

- Evaluate DTA Offset Opportunities: Assess whether DTLs can be offset against existing deferred tax assets.

- Incorporate DTL Forecasting into Strategic Planning: DTLs should factor into dividend planning and financial modelling.

🎯 Final Thoughts

Fair valuation brings transparency. But with it comes complexity.

Deferred tax liabilities may seem like a technical adjustment, but their impact can be far-reaching. From influencing board decisions to affecting investor perceptions and deal valuations, DTLs can significantly distort the financial story if not addressed strategically.

So the next time your asset revaluation adds a million to the top line, ask yourself:

Is a hidden liability quietly diluting your bottom line?