Why Don’t People Trust Audits? Because They Don’t Know SA 200

In a world driven by data, decisions, and disclosure, the role of an auditor has never been more critical. Audited financial statements are the cornerstone of investor confidence, regulatory compliance, and stakeholder decision-making. Yet, many fail to appreciate the invisible framework that makes audits meaningful, credible, and reliable.

At the heart of that framework lies SA 200 – Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with Standards on Auditing. Far from being just another technical guideline, SA 200 is the spine of the audit process, the standard that defines what it means to audit—and to audit well.

Let’s walk through why SA 200 matters, not just for auditors, but for every entrepreneur, CFO, investor, analyst, and business leader.

SA 200 is where the audit journey truly begins.

It sets the tone for independence, ethical behavior, and the exercise of informed judgment. In a time where financial manipulation can be sophisticated, SA 200 re-establishes what it means to audit with purpose and principle.

What Is SA 200?

SA 200 is the foundational Standard on Auditing (SA) issued by the Institute of Chartered Accountants of India (ICAI), aligned with the global International Standards on Auditing (ISAs).

Its purpose is straightforward yet powerful: To establish the overall objectives of the independent auditor and to set out the nature and scope of an audit conducted in accordance with SAs.

In essence, SA 200 answers three fundamental questions:

- What is the auditor’s ultimate goal?

- What principles guide their conduct?

- How do they navigate the complex terrain of financial statements, internal controls, fraud risks, and more?

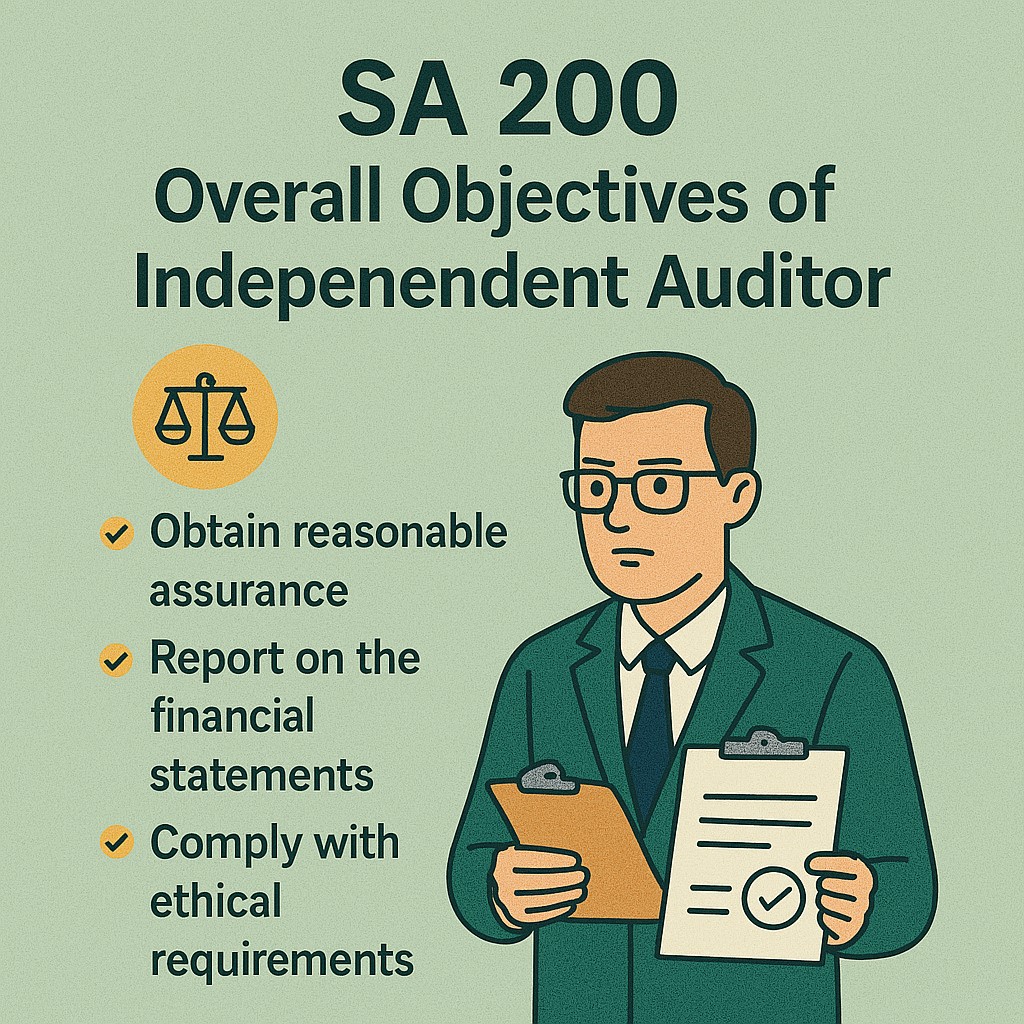

The Core Objectives Defined by SA 200

At the heart of SA 200 are the three core responsibilities of the auditor:

- To obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error.

- To express an opinion on whether the financial statements are prepared, in all material respects, in accordance with the applicable financial reporting framework.

- To report on the financial statements and communicate in accordance with the Standards on Auditing.

The Truth Behind “Reasonable Assurance”

One of the most misunderstood terms in audit reports is “reasonable assurance.” It’s often confused with “absolute assurance,” which the auditor is never expected (nor able) to provide.

This is a crucial distinction.

Due to the inherent limitations of an audit, the auditor cannot—and should not—guarantee that the financial statements are completely free of misstatement. These limitations stem from factors such as:

- The use of judgment in financial reporting

- The nature of audit procedures, which are often based on sampling

- The possibility of collusion or sophisticated fraud

- Limitations of internal control systems

- Time and cost constraints

Ethical Backbone: The Principles That Guide the Auditor

An audit is only as good as the ethical integrity of the professional conducting it. SA 200 lays down non-negotiable ethical requirements, including:

- Integrity: Auditors must act with honesty and straightforwardness.

- Objectivity: They must not allow bias, conflict of interest, or undue influence.

- Professional competence and due care: Auditors are expected to maintain professional knowledge and skill at a level required to ensure competent performance.

- Confidentiality: They must respect the confidentiality of information acquired during the course of the audit.

- Professional behavior: Auditors must comply with relevant laws and avoid any conduct that discredits the profession.

The Pillars of a Robust Audit: SA 200 in Action

To deliver a high-quality audit, SA 200 emphasizes five foundational elements that every auditor must uphold:

- Professional Skepticism: A mindset that continuously questions and critically assesses audit evidence. Auditors must be alert to conditions that may indicate possible misstatement and must exercise caution, especially in areas of judgment or estimation.

- Professional Judgment: Audit procedures often require making complex decisions—whether it’s about materiality, risk assessment, or evaluating the adequacy of disclosures. Professional judgment ensures these decisions are informed, consistent, and rooted in experience.

- Sufficient and Appropriate Audit Evidence: An audit opinion cannot be based on assumptions or management representations alone. SA 200 mandates that the auditor must obtain evidence that is both sufficient (enough in quantity) and appropriate (reliable and relevant in quality).

- Adherence to Auditing Standards: Auditing is not an art of free choice—it is governed by a set of standards. SA 200 insists that all other applicable Standards on Auditing (SAs) be followed diligently to ensure uniformity, compliance, and completeness.

- Risk Awareness: While SA 200 doesn’t dive into the details of risk assessment (covered in SA 315 and SA 330), it does highlight the importance of understanding the business, the environment, and internal control systems to design appropriate responses to audit risk.

Why SA 200 Matters for Businesses, Not Just Auditors

For many non-auditors, auditing standards may feel distant or overly technical. But SA 200 is one standard that every stakeholder should be aware of, because it defines the very quality and credibility of the financial information they rely on.

Here’s how it impacts different users:

- Founders and CFOs can understand what to expect from their auditors and how to strengthen their internal control systems.

- Investors can interpret audit reports with a clearer understanding of the scope and limitations.

- Lenders and bankers can trust that the audited financials are backed by a systematic and independent process.

- Regulators can rely on audit opinions that adhere to globally recognized frameworks and ethical codes.

Conclusion: SA 200 Is Where Trust Begins

In a world that’s increasingly skeptical of numbers, standards like SA 200 don’t just ensure quality—they build confidence. They enable auditors to serve as gatekeepers of financial truth and help businesses and investors make better, more informed decisions.

So, the next time you come across an audit report, remember—behind that opinion lies a world of rigor, judgment, integrity, and professional skepticism. And at the foundation of it all, is SA 200.

It may be the first in the list of auditing standards, but it’s the one that makes all others meaningful.

Is your business relying on audits that simply comply—or ones that truly stand for integrity?